Commodity, Until It Isn’t

Microns Result and The Rapid Transformation of the Semiconductor Memory Market

After experiencing a few semiconductor cycles, I began to wonder not only why there was a cycle, but also why something with a profound impact on the semiconductor industry was not studied in more detail.

The old hands told me not to worry. Things go up and down while we continue doing what we do: Two operational modes: 1. Screwing the customer. 2. Being screwed by the customer.

It has to be said, there is not much time to think in a semiconductor company. After you are conditioned to run on a diet of caffeine and cortisol, you are ready to enter the corporate hamster wheel and give your quarterly sacrifices of flesh and soul.

Semiconductor corporations are funny constructs. Exorbitantly paid executives are pretending to make a difference commensurate with their pay packages, while the rest of the organisation is pretending to comply.

Before you accuse me of being a disgruntled employee, I have to say that this industry gave me tremendous opportunities, and I loved my days as a corporate hustler, but I am also blessed that I got out in time to tell about it.

Everybody is pretending to cooperate while pushing their own irrelevant little piece of the puzzle forward, irrespective of what the corporate strategy of the day is.

You are not paid to think creatively - you are paid to pretend to comply!

Executive action (sometimes confused with strategy) can generally be categorised into two buckets:

We need to do something to increase the number this quarter.

We need to do something when 1 failed.

Not many minutes are spent on the long-term strategy. I remember a meeting where I was asked: “Do you mean short term or the quarter?”

Long-term strategy is something that happens to you while you are busy planning it.

Fortunately, the corporation is an ant hill full of intelligent ants moving their pet projects forward despite the stream of executive action. If the pet project succeeds, it will be remembered as part of the long-term strategy.

What looks like disobedience is really a mechanism to save the corporation from itself.

This behaviour is called management-layer dampening, in which each management layer dampens the impact of executive action from above. Both good and bad actions. While this is frustrating for senior management, management dampening has saved many corporations that have engaged in short-term, quarterly margin-grabbing practices that hurt customers and partners.

I really never understood the obsession with “making the quarter”. Every minute spent on making the quarter is taken away from “making the future”.

The problem with “making the future” is that it is a strategic exercise that requires information about the external environment and the current forces affecting it.

In my experience, this is difficult for semiconductor executives, as they have risen on their expert knowledge, which interferes with neutral analysis.

I was surprised that semiconductor leaders in general were always caught off guard by the downcycle and had to take decisive action on something that was predictable.

Preparing for the semiconductor cycle and intercepting it could give semiconductor companies a competitive edge. This is why I began analysing the continuous changes in the semiconductor industry

Soon, it turned into monitoring the entire semiconductor network, from upstream materials to semiconductor consumers near the end-customer ocean.

In the beginning, I was searching for small changes in the financials of the semiconductor supply network. I was down in the grass with my looking glass, observing beetles scuttling around, when suddenly they were all crushed by an elephant's foot.

It was time to put my looking glass away, as the AI meteor had struck and radically changed the semiconductor environment. The industry was no longer being impacted by ripples but by tsunamis that were tearing the supply chain apart.

The industry has now adapted to the rise of Nvidia’s AI servers to the point where I find Nvidia's revenue growth in the first H100 quarter cute.

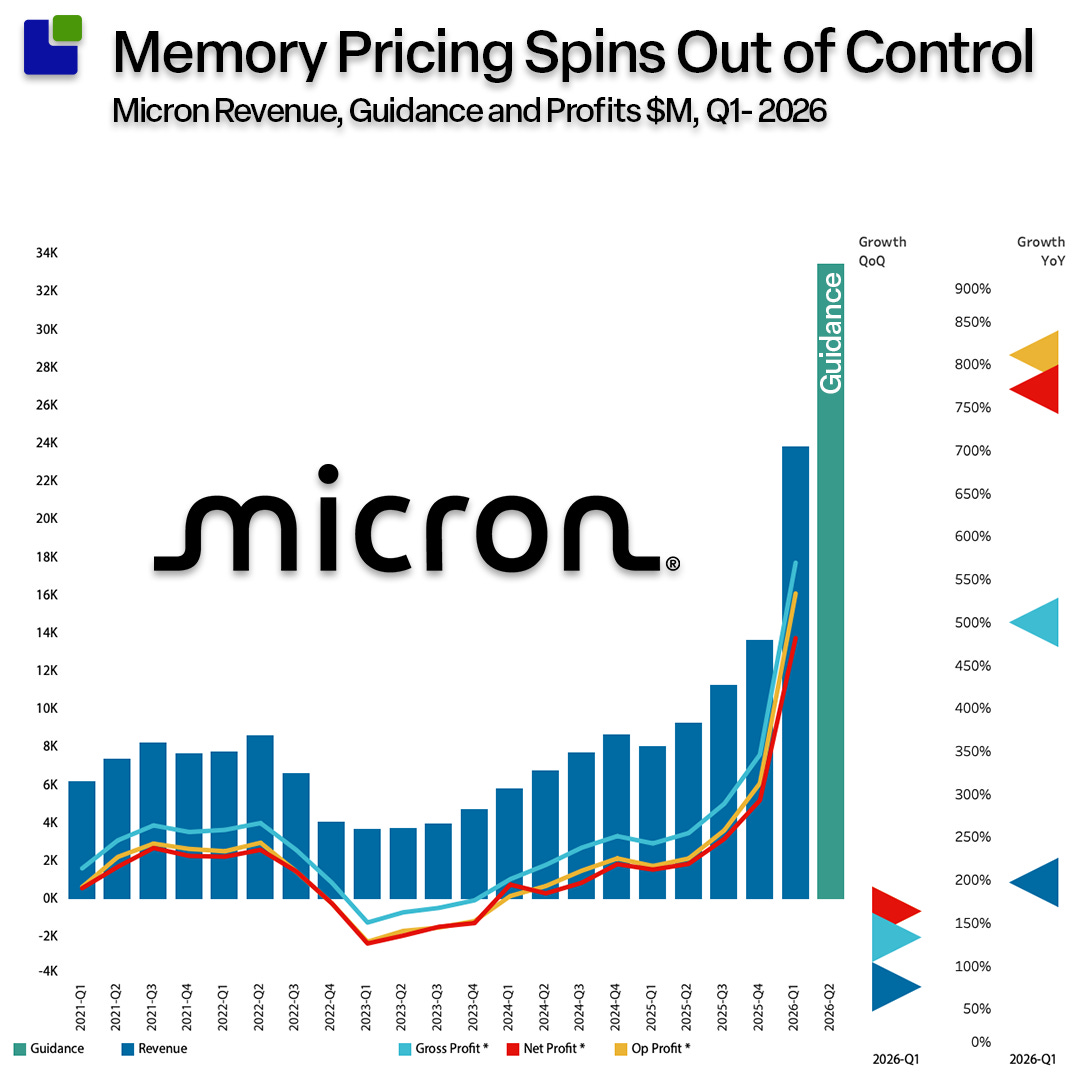

Adding over 5B$ in quarterly revenue used to be impressive in this industry, but now we need to get used to it. The AI revolution is now well into its second era of scarcity, as memory prices continue to rise and Micron just delivered quarterly revenue growth of more than $10B.

A common mistake in business analysis is ignoring the importance of magnitude and implications. The increasing memory prices are no longer news. Even people outside the industry understand this. Understanding that something is changing is entirely different from understanding the magnitude of the change and its implications. This is where I have my fun (sad - I know).

It is time to analyse the Micron result and its impact on the semiconductor supply network.

The Q1-2025 result of Micron Technology

The surprise is the surprise. While this sounds a bit funky, the large investment banks are doing their best to track and forecast memory prices and their impact on Micron’s results, but they were surprised. Micron was also surprised.

Micron delivered revenue of 23.9B$, growing revenue close to 75% QoQ and beating its own guidance by more than 27%. While the guidance numbers released by semiconductor companies are home-safe numbers with a bit of padding, a 27% beat means something changed dramatically in the quarter. For Micron, that variable was that memory pricing increased more than predicted.

The consensus revenue from the analysts, after removing this padding, is $20B, a 20% beat.

Lastly, I was surprised. If you are an expert, you are never surprised, but fortunately, I am a business analyst, so I don’t care.

This is the first insight of this post. From a customer perspective, pricing has deteriorated significantly, and we are now well into the next transformation of the semiconductor supply chain following the GPU transformation.

As the profits, especially the operating profit growth, jumped much higher than revenue growth, we know this is price-driven. While revenue grew nearly 3x YoY, operating profit soared to more than 9x that of a year ago.

The next surprise was the guidance. Micron expects to grow by an 48.7% next quarter, indicating that the memory markets can still tolerate more pain before closing their order books.

Micron expects demand to outstrip supply at least through the end of 2026 unless something dramatic happens in the world economy that the Trump administration is busy obliterating.

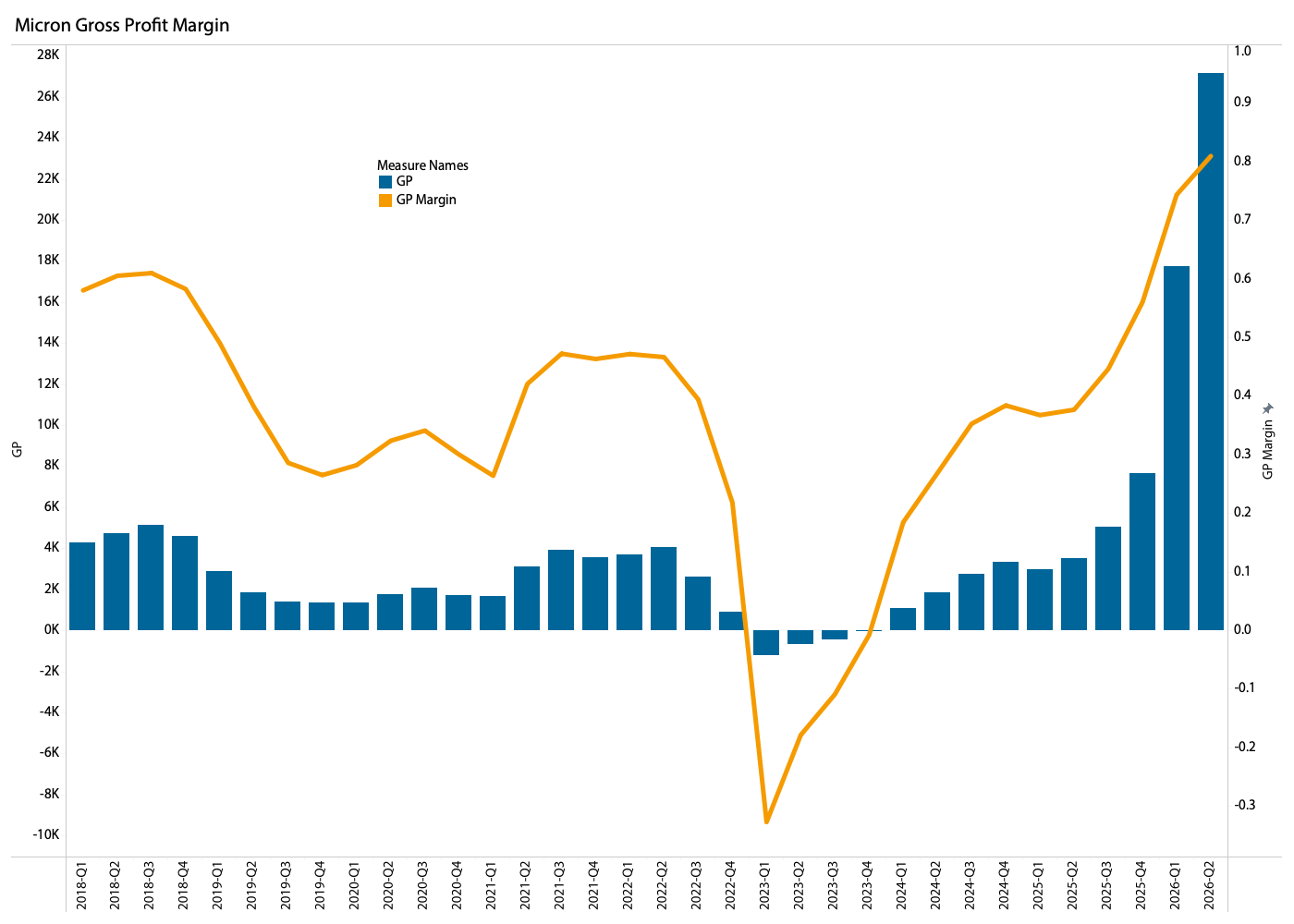

The impact on Gross Profit and margin is astonishing.

In Q2-26, another 10B$ of gross margin will be added if the guidance is met. Gross margins reached a record 74.4% in Q1-26, beating the previous record set during the 2018 upcycle. In Q2-26, the projection is 81%, up 2,000 basis points from the last record.

We are not only witnessing a dramatic upcycle but another structural change of the semiconductor market and its supply network.

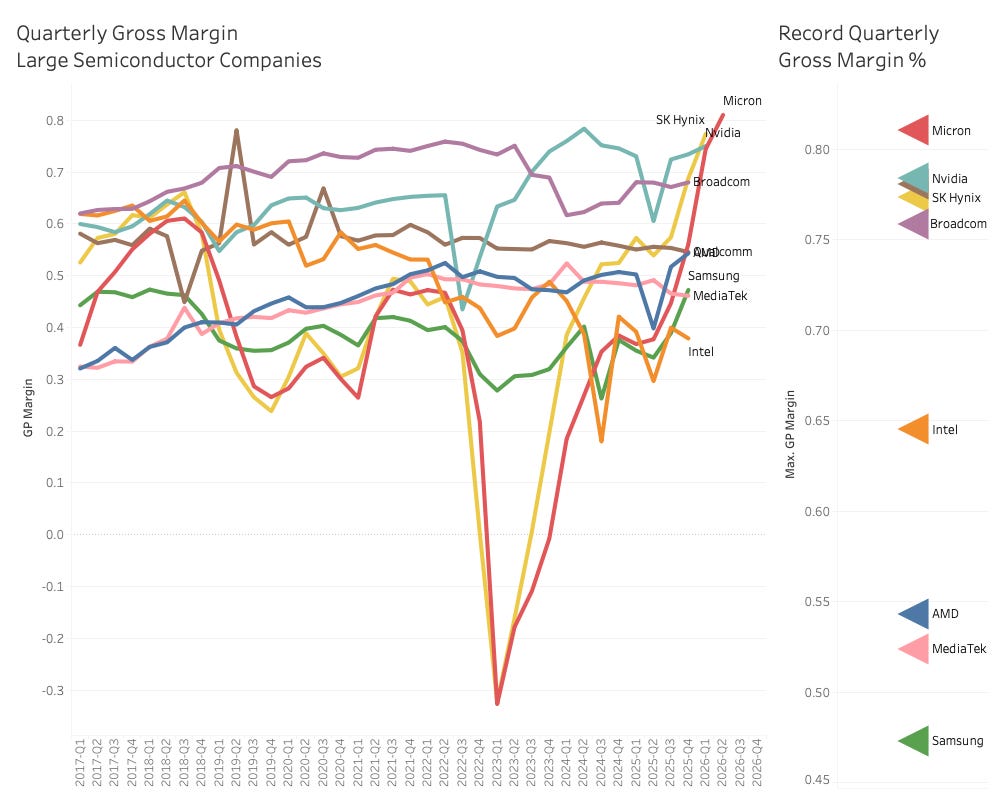

Without managerial supervision, I sometimes get carried away and need to verify my statements. The quarterly gross margins of the leading Semiconductor companies are shown below.

The current record was set in Q2-24 by Nvidia with 78.4% gross margin. In the 4th quarter of 2025, Nvidia was second at 73.4%, behind SK Hynix at 77.3%, already hinting at a structural change. However, if Micron meets its guidance, the company's 81% gross margin will be an all-time high for the semiconductor industry. That is, if SK Hynix does not deliver something even wilder in this quarter, which is plausible.

This is indeed a structural change. How long it will last is an entirely different matter.

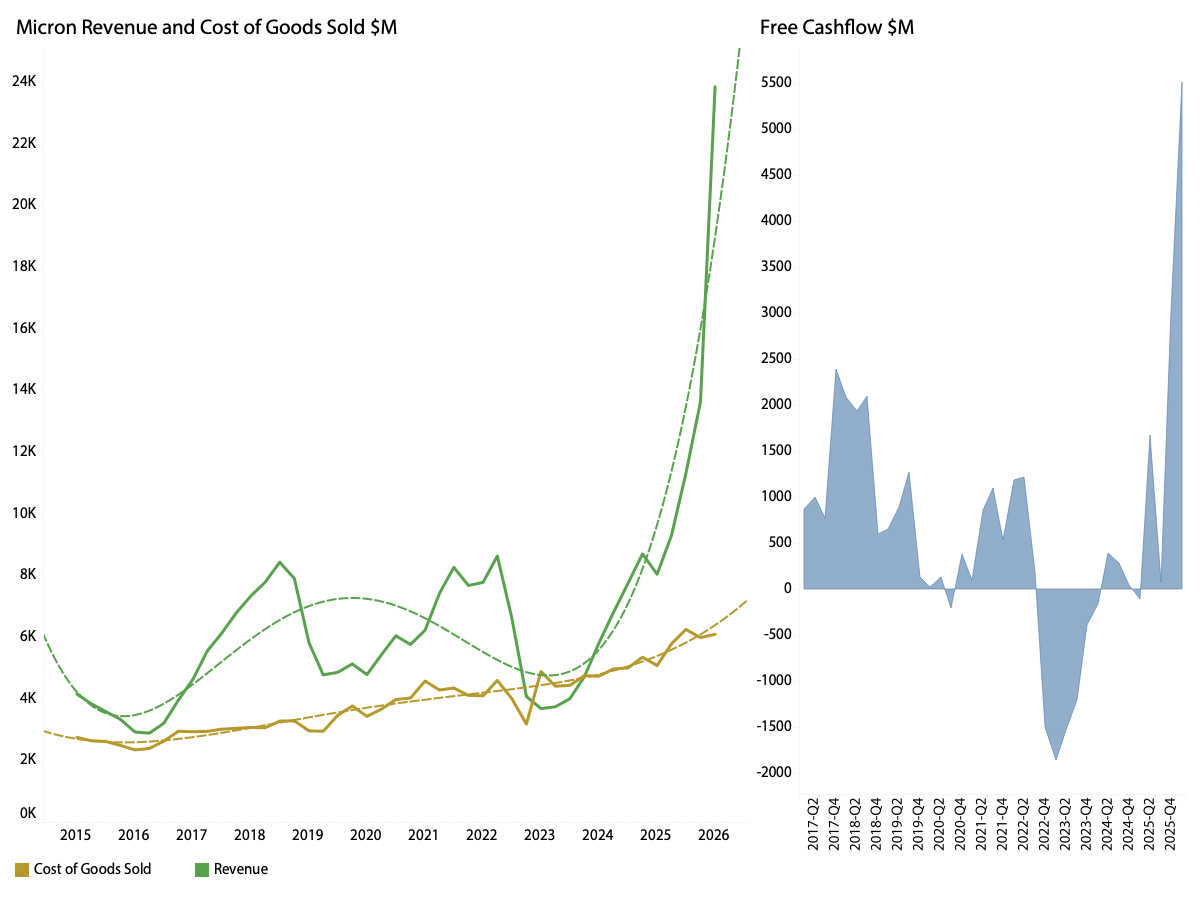

The exploding gross margins have a profound impact on Micron’s free cashflow as can be seen in the chart below:

As the Cost of Goods Sold is a good proxy for product volume shipped, it is clear that there was no meaningful increase in shipments. In fact, the Q1 shipments were still behind Q3-25 costs. Most of this is likely due to product mix.

The guidance for Q2-26 adds another 10B$ in revenue, and once again, this will be without a meaningful increase in shipment volume. In other words, Micron will have a lot of cash to spend even after giving its people fat bonuses and returning cash to investors through additional stock buybacks and dividends.

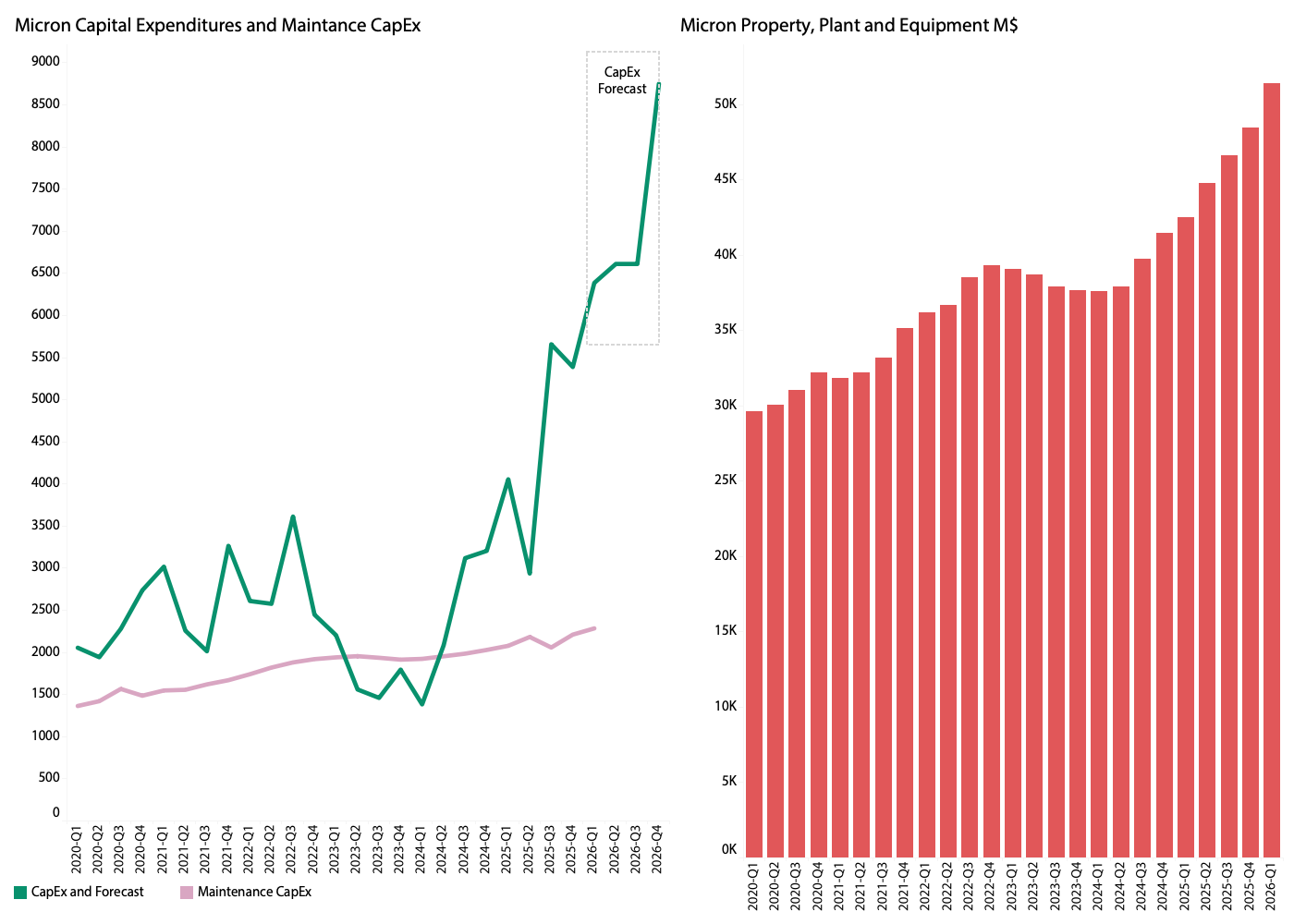

This is also needed because Micron, like the other large memory companies, underinvested during the last downcycle, as shown below.

It is hard to blame a company for lowering its CapEx investments when free cash flow is deep in the red, but this is the craftsmanship of memory companies. Survive staring into the abyss while filling it with dollars from the last upcycle.

The CapEx fell below the maintenance CapEx needed to keep manufacturing levels, and the capacity measure in Property, Plant and Equipment declined over two years, laying the foundation for the scarcity we are seeing now.

While the CapEx forecast points to a significant increase, most of it will not materially impact 2026 capacity; more likely, it will cause the next downturn (if that is still a thing) 12 to 18 months from now.

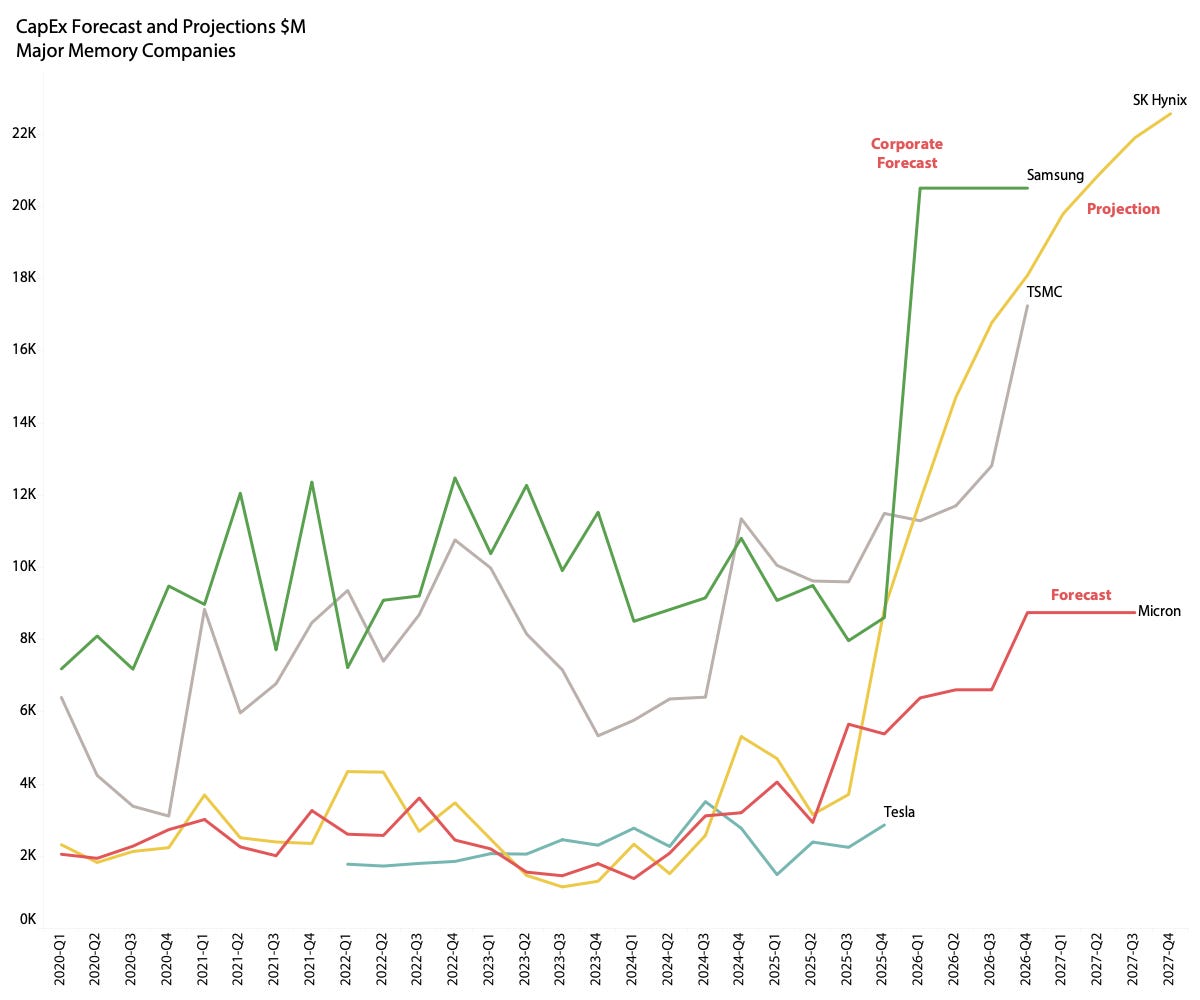

The CapEx will grow from $15B in the last fiscal (Q3-Q2) to $25B this fiscal and $35B next fiscal. While this is a significant increase and represents more than a 52% CAGR, it must be viewed in light of Micron’s two major competitors and a couple of other randomly selected companies.

While Samsung's CapEx forecast is corporate, the vast majority will be ploughed into semiconductor manufacturing, specifically memory. The SK Hynix CapEx projection is based on Consensus revenue and the company's stated commitment to maintain the current CapEx-to-Revenue ratio.

Micron is up against a formidable CapEx budget and will need to pump the marketing budget a bit in the direction of being “The only U.S.-based manufacturer of advanced memory products”

With less than 18% of its fixed assets and 20% of its headcount in the US, this is a truth with modifications, but understandable in the current political environment.

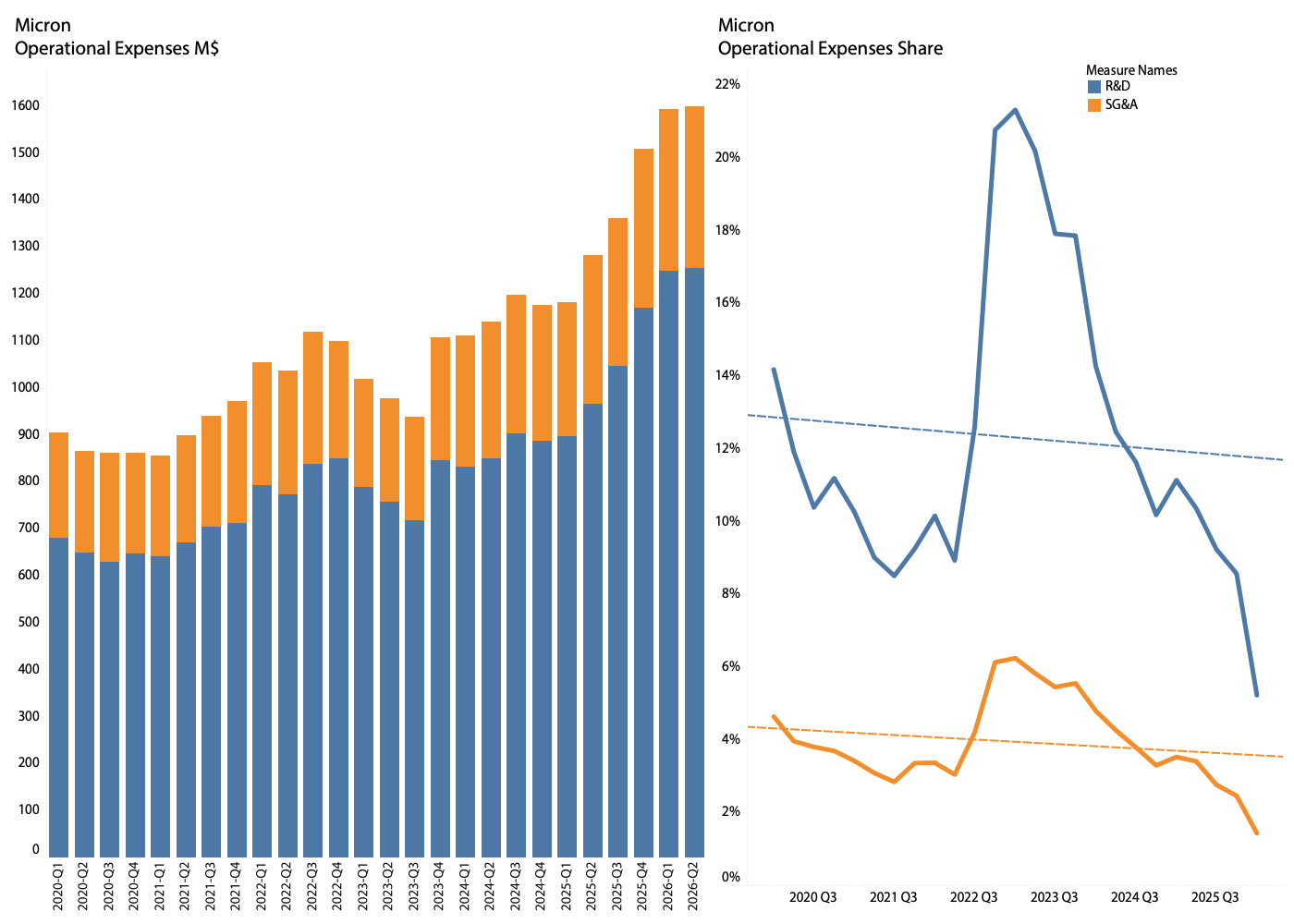

Apart from investing in CapEx, Micron also wants to make a meaningful increase to the R&D budget, although the immediate quarter will be at the same level as last.

While steady R&D budgets are needed, they should be viewed in the context of the business. The operational cost as a share of revenue has declined dramatically since the downcycle and is now at an all-time low of 6%, as shown in the chart.

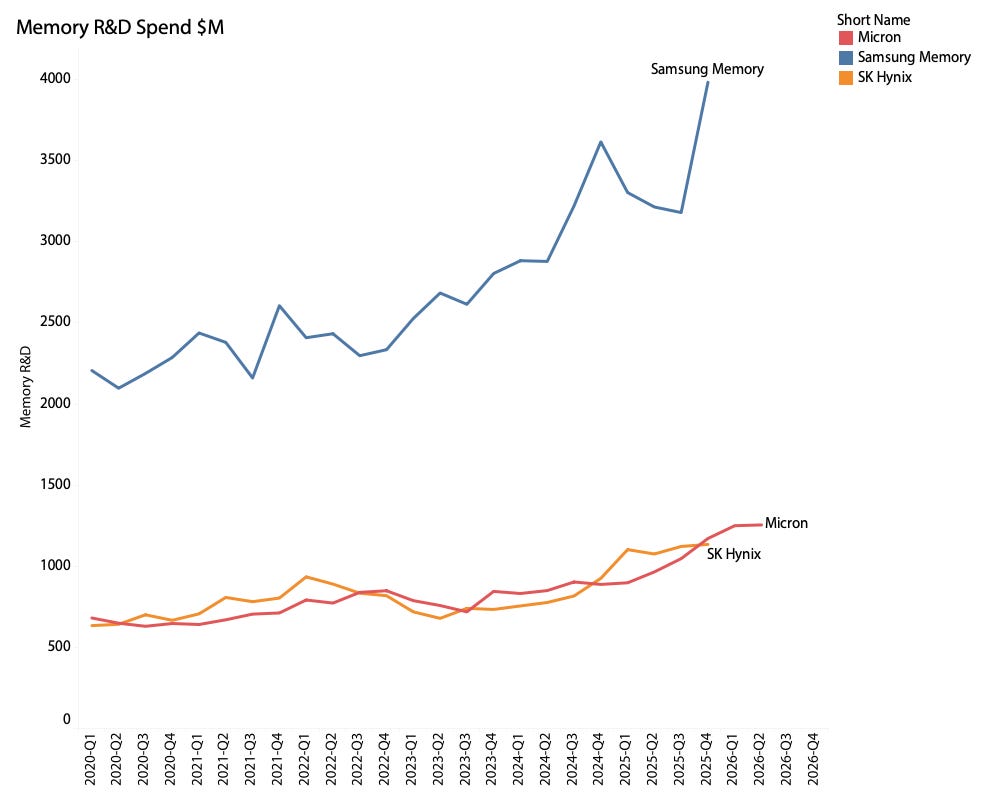

Also, regarding R&D spend, it is necessary to compare Micron’s spending with that of its large competitors.

Currently, Micron has R&D spending very similar to SK Hynix's, and, quite impressively, both are competing effectively with Samsung, which has a much larger R&D budget. The Korean conglomerate currently spends about half of its corporate R&D budget on memory, a testament to the fact that money spent does not always yield proportional results. Samsung certainly still has many internal problems to address, even though the latest result is much better.

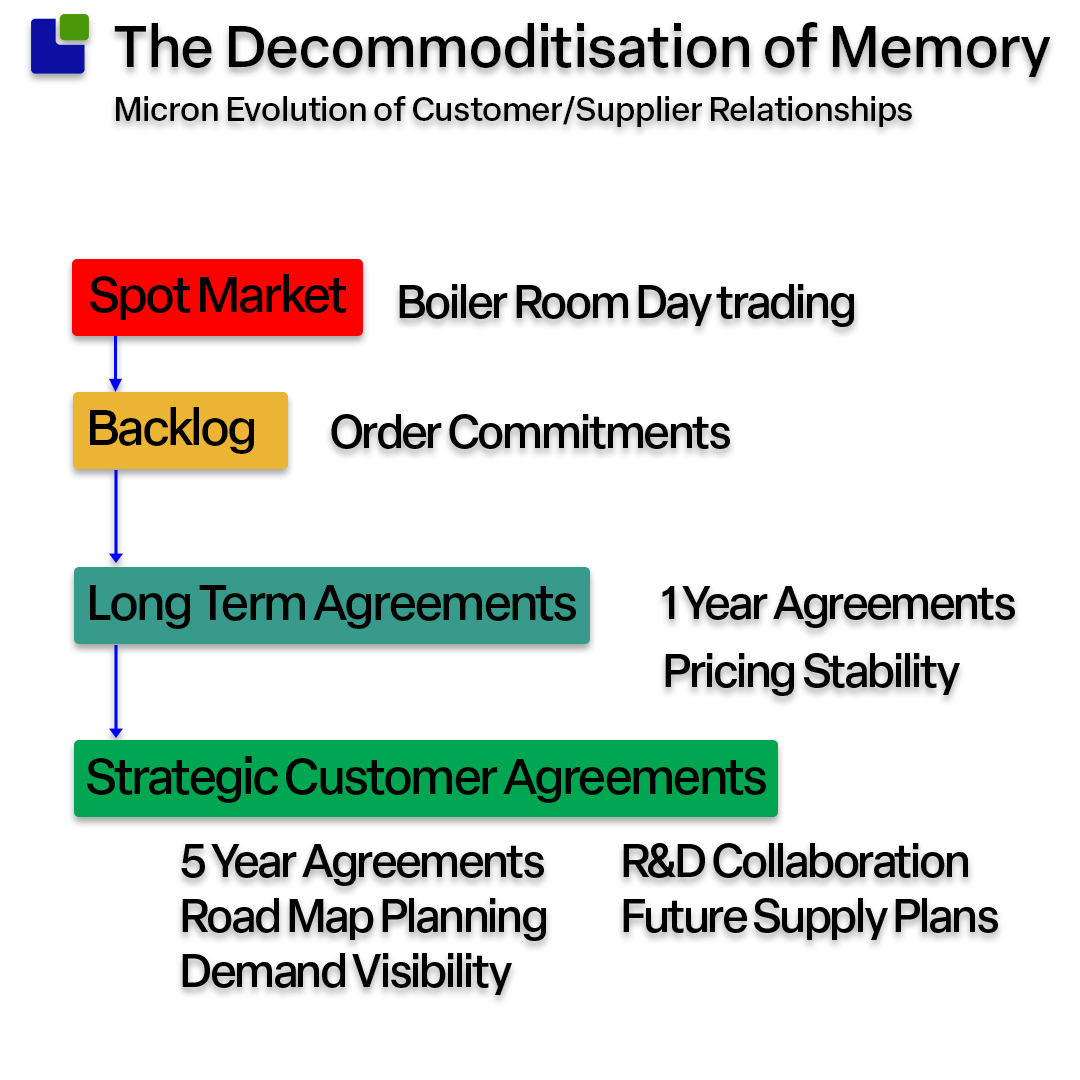

Before diving into the demand and supply situation, the Micron investor call unveiled a very interesting development in the relationship between memory suppliers and consumers: The Strategic Customer Agreement (SCA).

Traditionally, memories were traded as commodities in a boiler room-style setup. Although I did not directly work as a memory day trader, I have had colleagues doing this gruelling work - they did not last long.

The main customers were PC manufacturers that more or less directly passed the memory pricing through to the end products. As memory evolved into serving other markets, the normal industry order/backlog structure was introduced for those markets, often with clauses that should memory pricing swing more than expected.

With the emergence of high-bandwidth memory, memory companies eyed a chance to exit the lethal memory cycle by entering into fixed-price agreements with the few large consumers of HBM, predominantly SK Hynix, AMD, Broadcom, and the large cloud hyperscalers. The LTAs have most recently been expanded to cover more than just HBM. They now include all memory requirements of the principals.

With the introduction of the SCA, the memory market is set to change dramatically, as the agreement involves far more than supply and demand, and an SCA will always get priority.

This gives Micron the opportunity to plan well into the next upcycle with some degree of supply and pricing protection while it secures the principal's supply. irrespective of product type and market situation.

The battle for GPUs has turned into the battle for memory, and with the first SCA, it might already be over. While Micron declined to name the customer, other financial analysis makes it quite obvious who it is.

The demand and supply situation

One of the problems memory companies face when planning capacity is that there are not only one but two memory cycles. While both NAND and DRAM follow (create) the general memory cycle, they deviate for periods, as can be seen in the Micron price trends below.