Finding Something to Bitch About

Men in Shorts and the Nvidia Q1-26 result

Most of the so-called “analysis” on Substack on LinkedIn is written to make a fast buck, and I am no different. I rely on Substack to survive to write another day.

The most profitable Substacks are giving stock advice on tech stocks by either pumping them or betting against them while pretending to be “analysing” the stock.

When you make money from a certain outcome, you are no longer analysing. You are shamelessly promoting a story that will make you wealthier.

While I certainly have holdings in Nvidia and the other companies I write about, I only bought Nvidia once, a couple of decades ago, and I never let my holdings get in the way of my analysis. I am also so fortunate that my holdings are not sufficiently large to tempt me to corrupt my principles.

My view of the stock market is that it has become narrative-driven rather than driven by fundamentals, and the short-term movement of stock is completely random. I know day traders will disagree, and I am ok with that. The narrative-driven stock market enables people with a large following to sell a story that aligns with a bet they have made.

I call them the men in shorts, and their stories get crazier over time as they increase their bets against a stock. One of their favourite bets is against the AI revolution in general and Nvidia in particular. The black-and-white approach is well-suited to social media and effectively ensures their posts reach the right audience.

I have no clue whether Nvidia stock will go up or down as a result of these black-and-white narratives, nor do I know whether the long-term investments of the large hyperscalers will yield a healthy return. From an analytical perspective, I don’t care. I will follow the AI revolution wherever it goes. Up or down or to hell. I am interested in extracting insights from the facts we are presented with to help people in the semiconductor supply network navigate their implications.

If you are one of my regular readers, you are used to my boilerplate statement before writing about Nvidia, as I will once again sound like a fanboy, because Nvidia delivered a way better result than analysts expected.

I woke up early to read Men In Shorts Monthly. The shortsellers were terrified over the result and were desperately trying to catastrophise the numbers with headlines like: “The three things Nvidia did not tell you..” or “The Nvidia financials that show the increased risk……”

While I agree that the risks have increased, this is more a result of Nvidia’s success than anything else. A potential revenue fall could be deeper than last quarter. $11B deeper, as this is the amount Nvidia added in Revenue this quarter. More than AMD’s total revenue in the quarter. Adding the revenue of your largest competitor is what I would designate as a high-class problem.

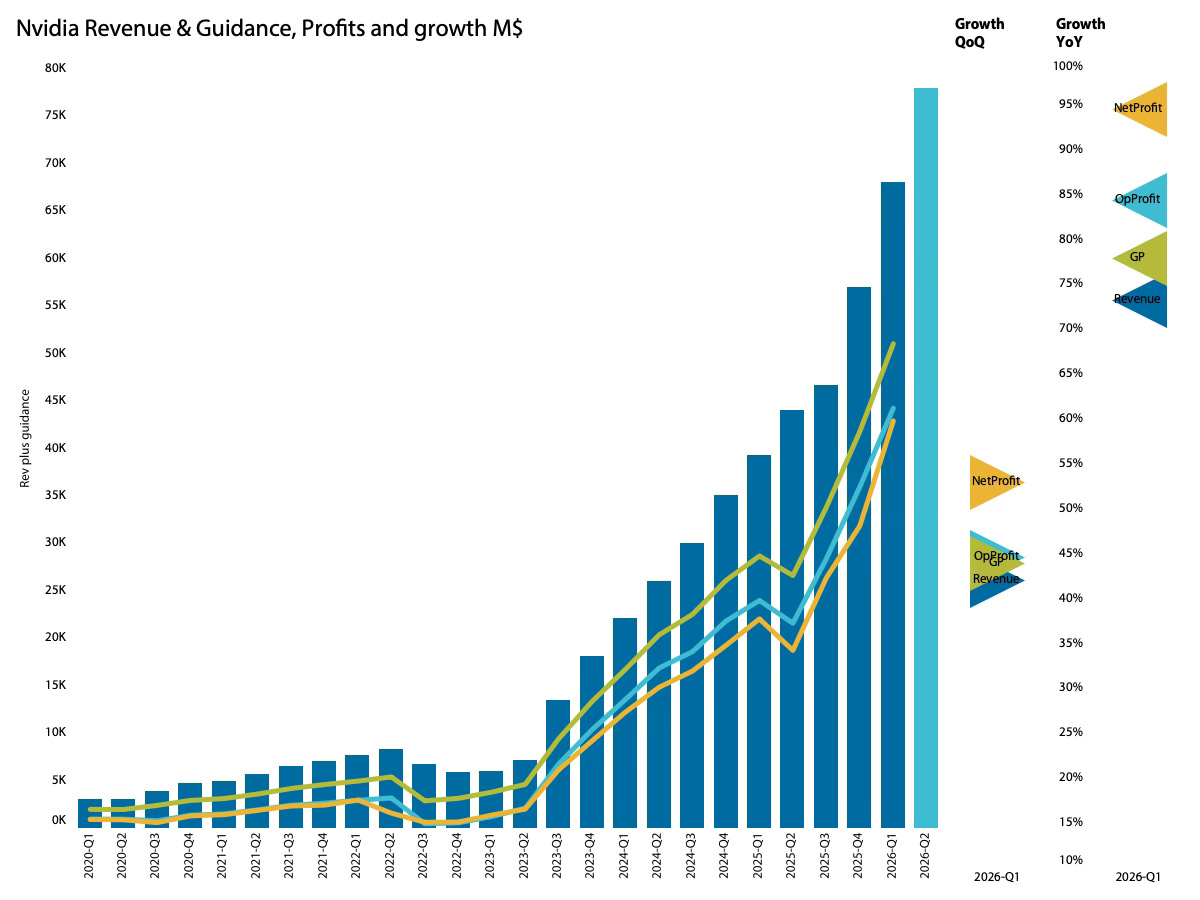

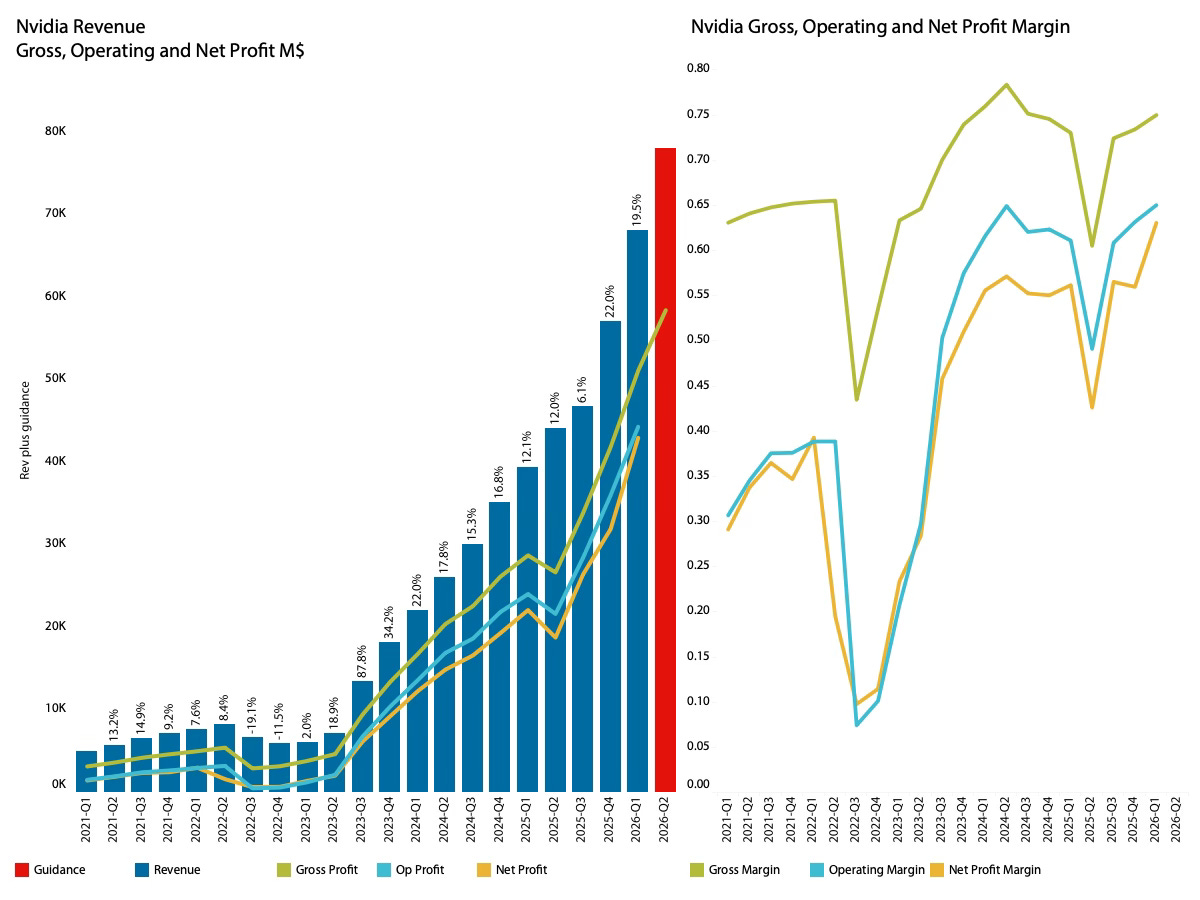

The Nvidia result

With revenue of $68.1B, Nvidia significantly exceeded the guidance of $57B. The 4.8% beat and 19.5% quarterly revenue growth are outstanding results, and they will make the short sellers' bets worse.

The men in shorts celebrated briefly as Nvidia stock fell below $185, but they crept back under the warm blanket as the large financial institutions increased their price targets to an average of $262.

More impressive was Nvidia’s guidance for Q2-26. The $78B guidance exceeded the analyst consensus revenue for Q3-26. In other words, Nvidia just beat the analyst by a full quarter.

All profit metrics outpaced revenue, indicating the maturity of the product pipeline despite the annual architectural shifts. Most impressive was the net profit growth of 34.6% QoQ and 94.5% YoY. NVIDIA has increased its quarterly profits by $20.8B over the past year. The total net profit of all semiconductor companies excluding Nvidia in Q3-25 (the last fully resolved quarter) was $37B.

While the guidance growth of 14.5% is lower than the current rate, it is safe to assume that Nvidia has some cushion and is planning to deliver more growth if the quarter progresses as projected. More about that later.

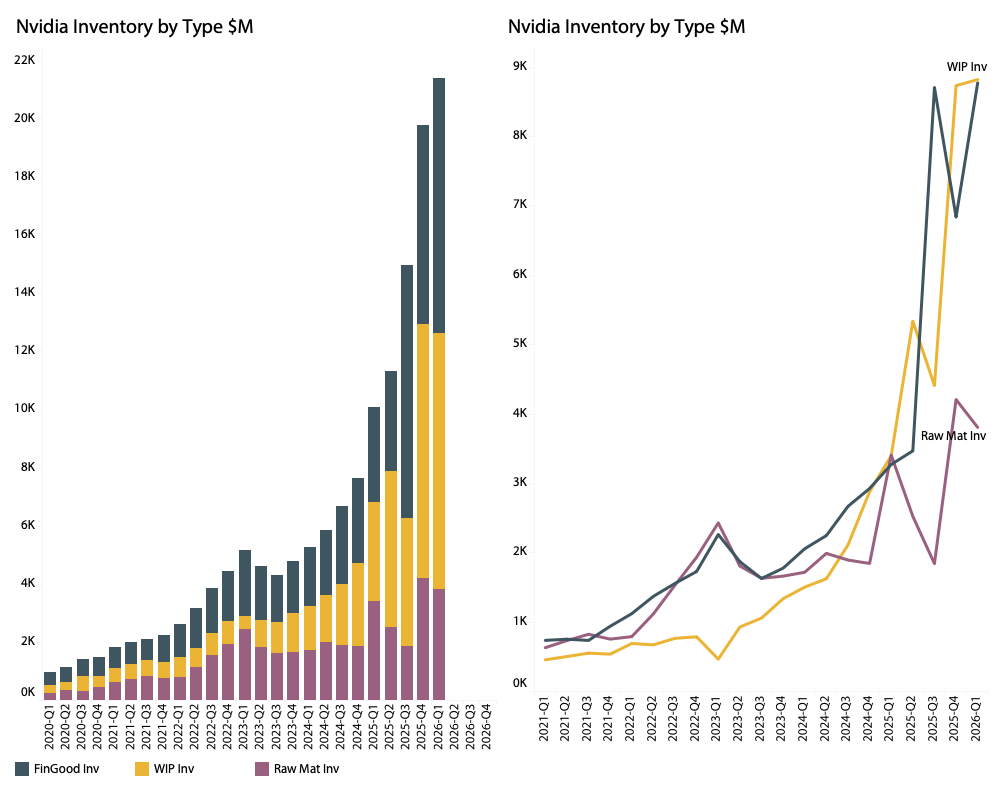

Apart from strong profit growth, most other financials were in line with revenue growth. Inventory growth was higher YoY but lower than last quarter and appears under control despite the increase in activity.

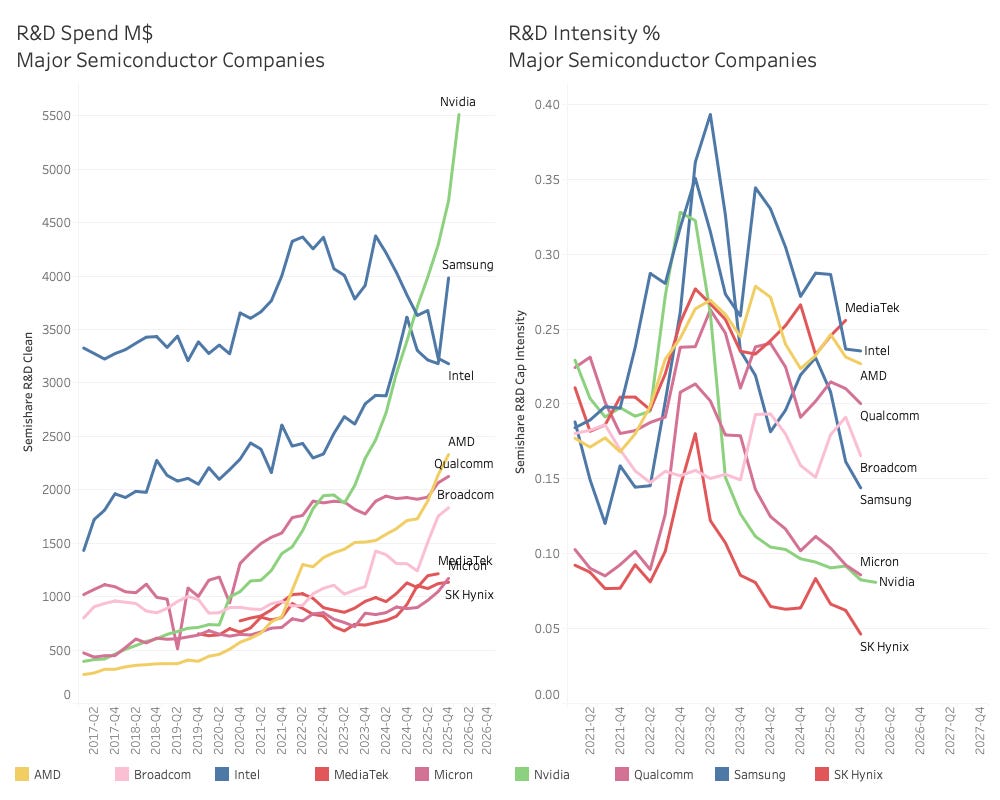

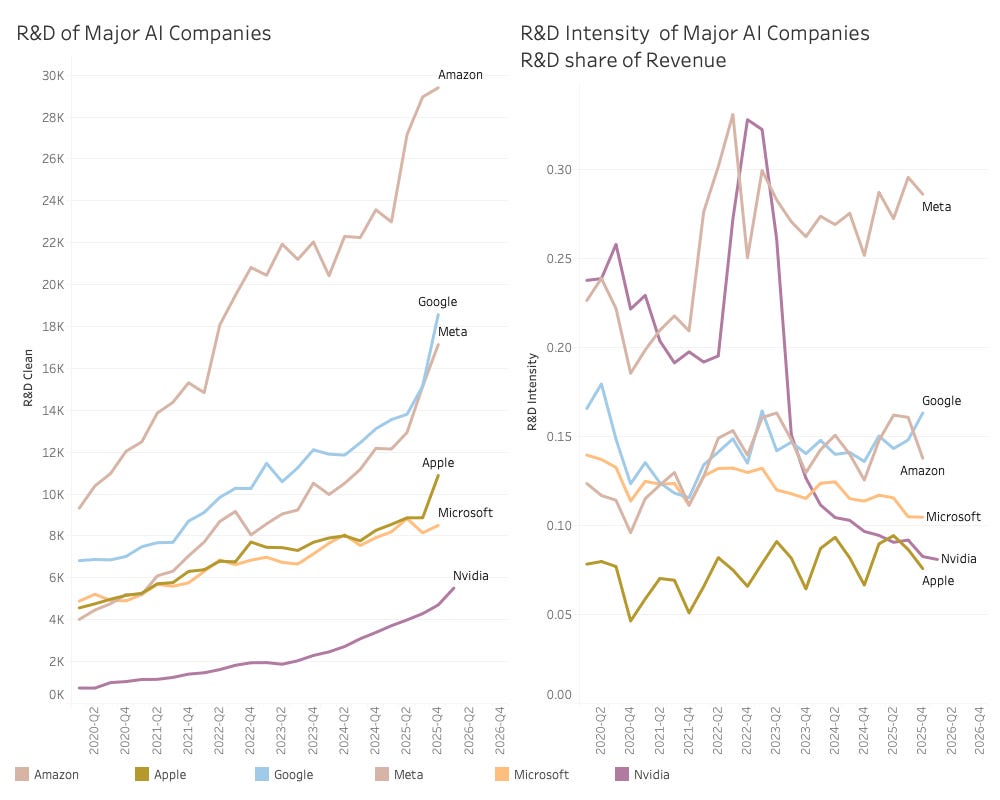

NVIDIA management made a point about its R&D spending.

Our pace of innovation, particularly at our scale is unmatched, fueled by an annual R&D budget approaching $20 billion and our ability to extreme co-design across compute and networking across chips, systems, algorithms and softwares, we intend to deliver X factor leaps and performance per watt average generation and extend our leadership position over the long term.

While high R&D spending is not a guarantee for success, it is a prerequisite. To win in Semiconductors you need to invest significant amounts of money in R&D.

The R&D spend of Nvidia and its peers can be seen below:

After an R&D level of around $2B/Qtr before the rapid rise of the H100 business, Nvidia is now outgunning all other semiconductor companies with a 5.5B$ spend in Q1-2026.

The intense revenue growth has lowered the R&D share of revenue from a peak of 33% down to 8%. Only SK Hynix has a lower R&D intensity.

Not only does Nvidia have a strong moat to defend its business, but it is also outspending any potential challengers amongst its competitors.

As Nvidia also compete with its customers, especially the large hyperscalers, the threat can also come from them.

While the large cloud companies still have larger R&D budgets than Nvidia, the GPU leader is making inroads, and it is implausible that any of the hyperscalers have a hardware development budget comparable to Nvidia’s.

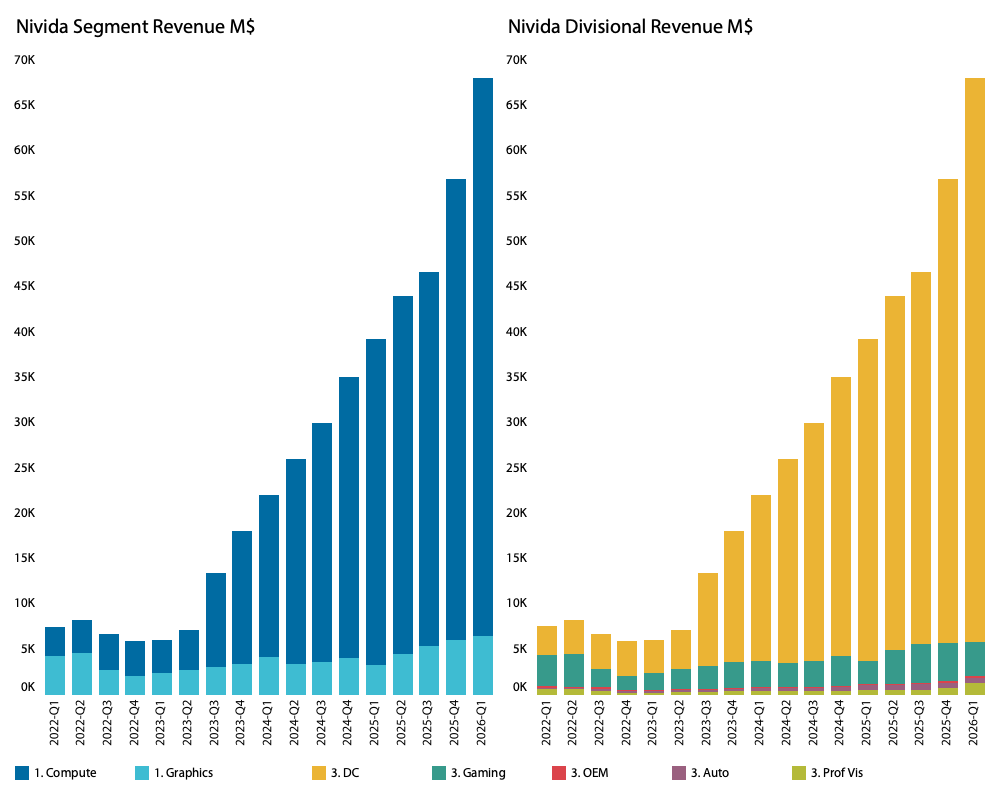

Revenue by segment and division is shown below.

To noones surprise, the trend of Compute and Datacenter growth continues. More interesting is the increase in revenue from professional visualisation. The division delivered a significantly stronger result than the corporate, with revenue growing by 74% QoQ and 159% YoY.

This is tangible evidence of the success of the Blackwell RTX PRO GPUs in Graphical workstations, representing a new front against AMD and Intel. Also, DGX Spark, the Mac-mini-sized personal AI supercomputer, is in the segment but is likely not behind the significant increase.

More interesting is the revenue by product: