Intel's Mountain to Climb

A review of Intel's strategic situation

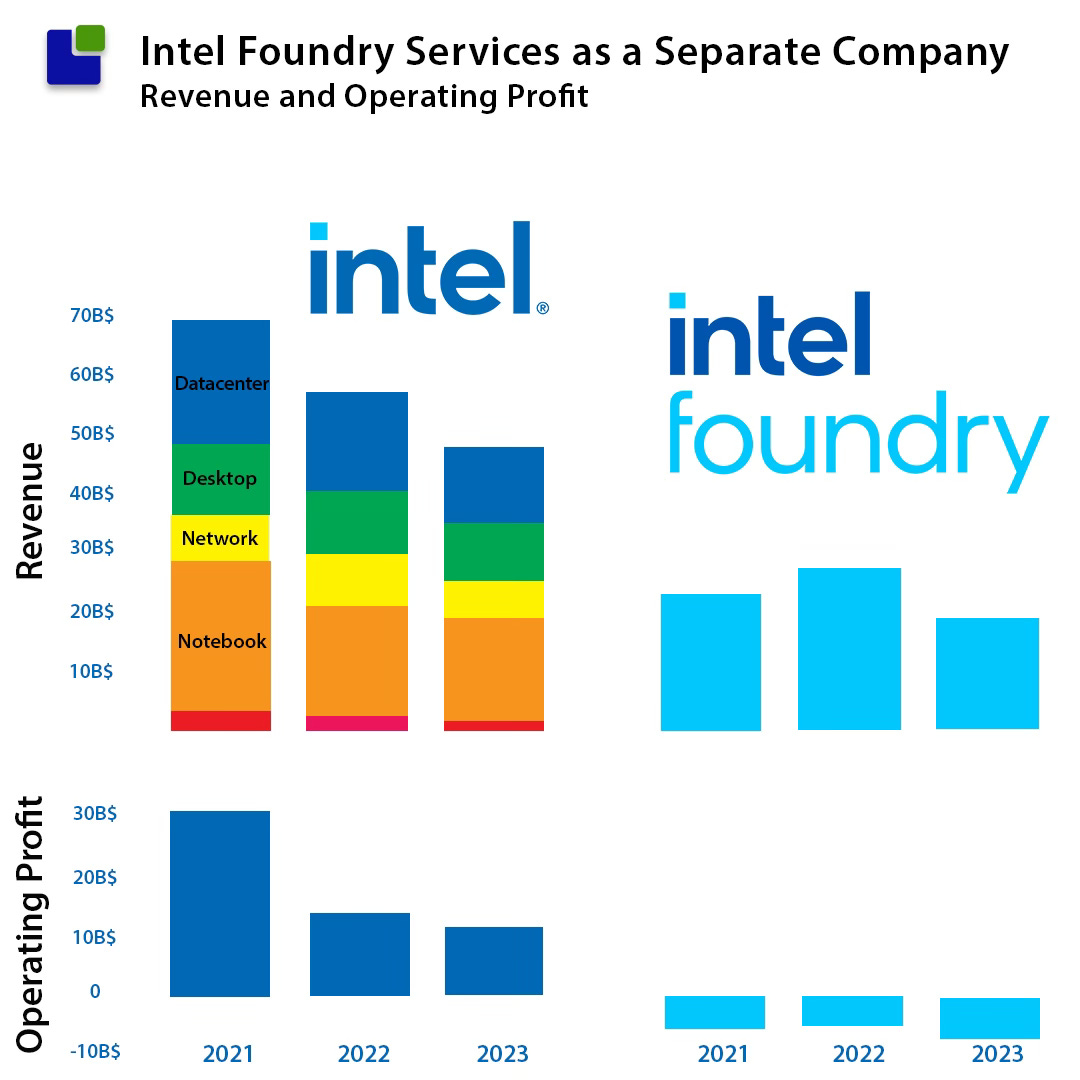

Intel is undergoing a significant strategic shift from being predominantly a product company with manufacturing to have two distinct strategic business areas. The company is untangling the manufacturing part from the product part by creating Intel Products and Intel Foundry Services (IFS).

From a strategic perspective, this is an ambitious move that is new to Intel. The company, used to being the 500 pound gorilla in the semiconductor market, has been used to being far ahead and dictating the rules of the industry. Both from a product and a process technology perspective.

The strategic move might be ambitious but it is also driven out of necessity. Intel’s financial performance has been subpar lately, not something the company or its stakeholders are used to.