Micron capacity constrained with record inventory?

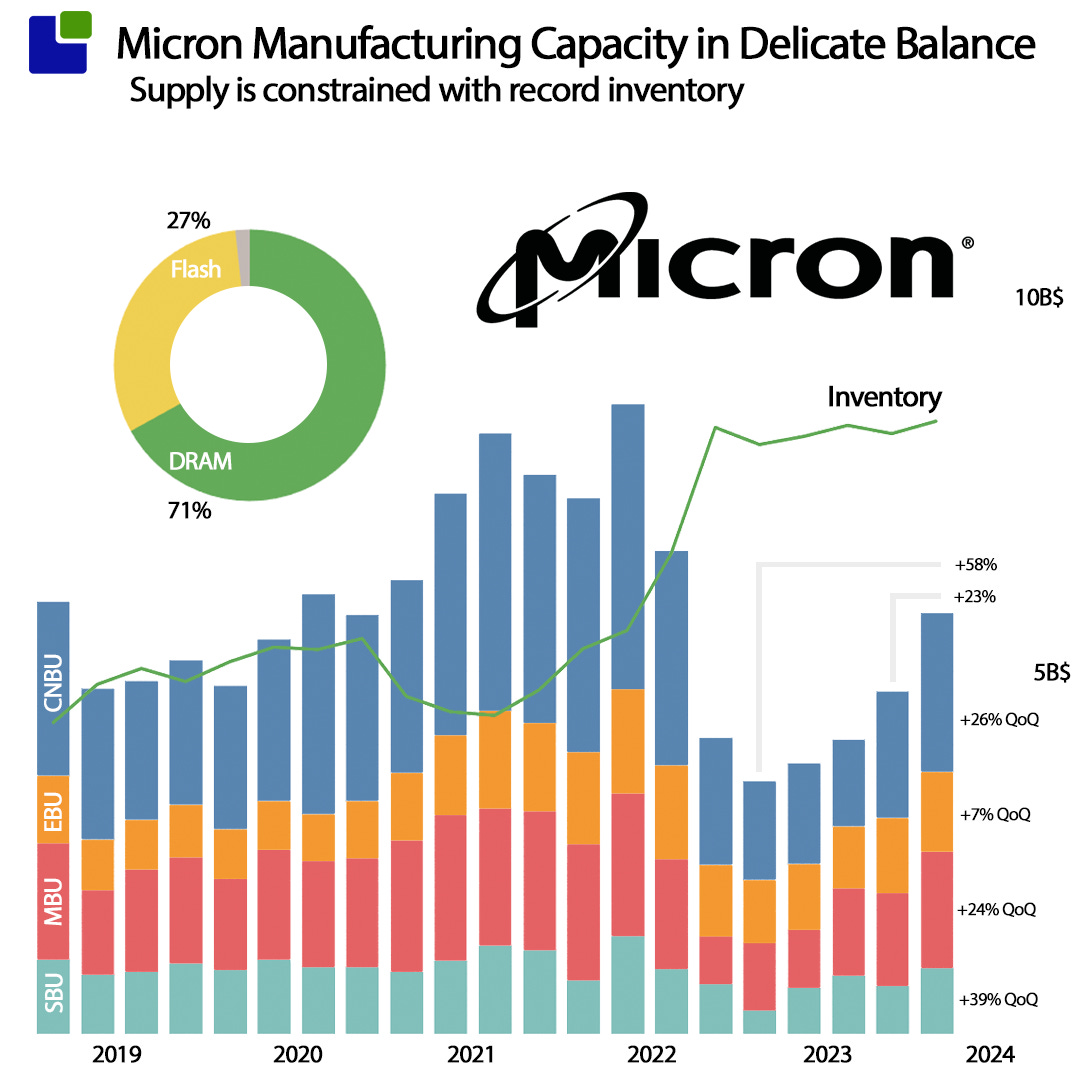

Micron just reported a strong quarter with 58% year over year and 23% sequential growth. The Company easily beat the earnings expectations. Reported EPS was $0.42 wile expectations were $-0.27.

In the investor call, Micron pointed to the strong growth of the datacenter and cloud business:

AI server demand is driving rapid growth in HBM, DDR5, and data center SSDs, which is tightening leading-edge supply availability for DRAM and NAND.

AI was also featured with a strong emphasis on HBM3E and the limited capacity means 24 and most of 25 production is allocated to customers. This was also the focus of most of the analyst questions. Micron refrained from quantifying the size and outlook of the HBM3E business although bait was laid out.

We are in the very early innings of a multiyear growth phase driven by AI as this disruptive technology will transform every aspect of business a…