The Corporate Combover

or an Update of the Semiconductor Tools Market

For the pure, there is nothing to hide.

And now to something completely different: The communication strategies of Semiconductor tool companies.

As the CEO’s of corporations are transforming into god-like figures, matching their god-like compensation packages, they also lose the very human quality of failing.

It all begins with small adjustments. When the internal analysts present numbers that challenge the glorious narrative of the Dear Leader, they will be told they are wrong, and HR will use the “Difficult” stamp in their loyalty ledger.

A new analyst with more palatable numbers will be promoted to the CEO's court, and the numbers will be used in the corporate communications.

Selecting the data to show is not really lying. Handpicking the most palatable “independent” data that puts the corporation in the best possible light is just part of the business of running a semiconductor tool company.

What begins as a small inconsistency can turn Trumpian, and the Dear Leader will tell people bringing the reality to the court, to “bury that shit”.

The investor call now turns into a Corporate Combover. Covering the bald spots with a layer of Corporate Candyfloss.

If the data selected to support the glorious narrative continues to turn negative, it is time to get rid of it, as it is obviously confusing the investor community ( = the stock price is going down).

Unfortunately, business data is like Crack Cocaine for the investor community. They only want more and get withdrawal symptoms if the data is not continued.

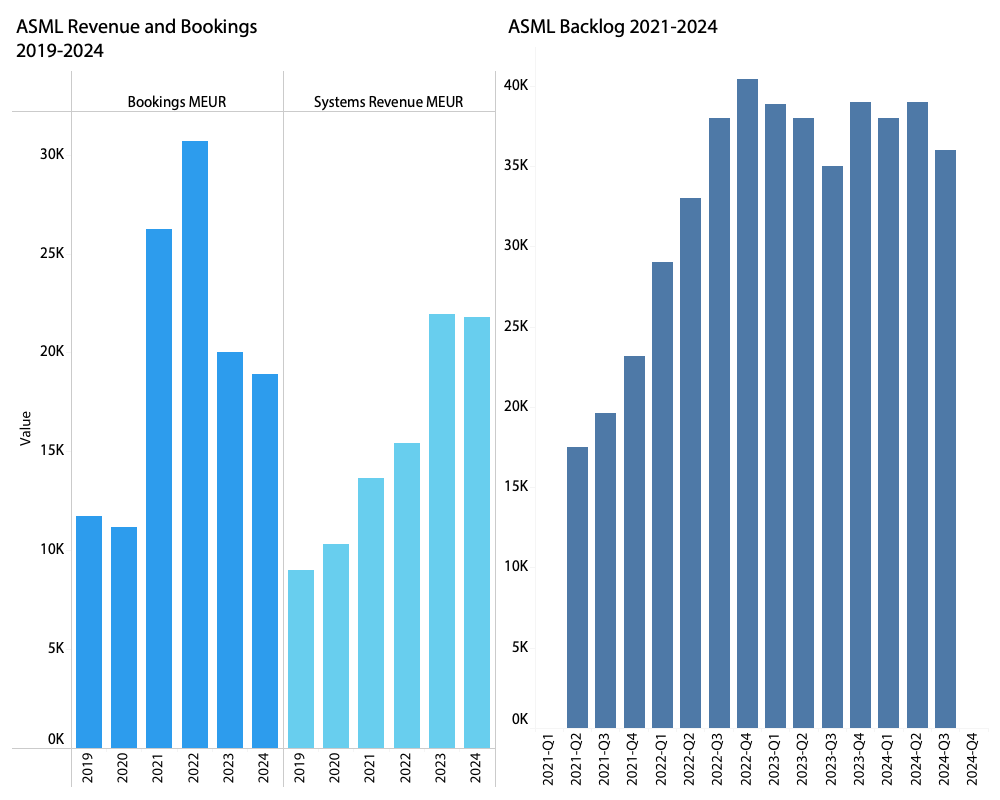

A few quarters ago, ASML signalled that it would discontinue order intake information as it was a weak real-time indicator given the long lead times. Rather, investors should trust ASML to convey the sentiment from customer conversations.

The attempt to replace data with more corporate candyfloss was met with contempt from the investor community and seen as a reduction in transparency.

While ASML kept reporting booking numbers throughout 2025, it remains on the chopping block and will be “de-emphasised” over time.

Not surprisingly, the decision to help investors “avoid confusion” came at a time when the Backlog and booking numbers looked less than glorious.

It could signal that a less transparent leadership culture was emerging at the same time as ASML got a new CEO. This could be a coincidence. Also, a possible coincidence was that the subsequent continuation of bookings disclosures through 2025 was joined by very favourable bookings and backlog numbers.

While I have great sympathy for the CEOs’ lack of enthusiasm for giving guys like me the firewood to roast them, they are leading public companies and should wear their big boy pants.

We already know that not everything is going north all the time. When things go south, a CEO of a public company should own it, let us know why it is happening, and what the plan is to address it.

Discontinuing the numbers is to me a signal that the bald spots are too large to be hidden by a corporate combover, and an unhealthy cult culture could be emerging. I will let you form your own opinion.

If you have followed my blog, you will not be surprised to learn that this is my introduction to something else that is going on.

And once again, it is shockingly coming from another Dutch company. While I could have said "European," you should understand that "Europe" is a geographical region. If you think a European culture exists, think again.

My international audience will not know the intricacies of the small Kingdoms of Northern Europe, but the Danes and the Dutch are generally very compatible and more scared of floods than avalanches. While Denmark has been conquered several times, the friendliest conquest was by Dutch farmers, who could not believe how cheap the fertile, flat Danish farmland was. The open and honest people had no problem integrating into Danish society, and only their funky names, different from our funky names, revealed their origins.

We would trust a Dutchman with our wallet.

While transparency and honesty are not the same, the concepts are closely related. If you are honest, you should not have a problem being transparent.

So it is surprising to me that ASM International is now trying to pull the same stunt:

You could think the good people at ASMI had learned their ASML lesson and chosen a good time to lower transparency, but no such luck.

While I don’t know if there is a slide of ethics culture within ASMI, the company is providing us with less information to verify the business’s health. This makes it easier for management to manoeuvre without raising questions, but it also encourages them to talk about the company's glorious future without any evidence.

If you are a stakeholder and have to choose between two companies, all other things being equal, you should choose the most transparent one. It doesn’t matter if you are an employee, an investor or a customer; you should always choose light over darkness.

Before medics find blood in my caffeine stream, it is time for an overview of the Semiconductor Tools Market.

The State of the Semiconductor Tool Market

From obscurity, the largest Semiconductor tool companies have been propelled onto the geopolitical stage as politicians have begun to realise that the future of the Semiconductor Industry is deeply reliant on a few companies capable of juggling atoms and photons.

The Light Magicians at ASML in the Netherlands and the Atom Engineers at AMAT in the USA are now well-known companies among politicians, duty officers and retail investors.

Intel's failure came as a surprise to the US military and the US government, which realised that a conflict with China over Taiwan would eradicate the US military's semiconductor supply chain.

While TSMC’s leading-edge manufacturing was superior, Samsung, later Intel, and Rapidus would also be able to manufacture leading-edge semiconductors.

What all of these companies had in common was the reliance on Extreme UV Lithography tools from ASML. While AMAT is equally important for the Semiconductor industry, it was not a chokepoint like ASML.

In 2019, the US administration persuaded (there was such a time, and yes, it was the first Trump administration) the Netherlands to bar ASML from selling its most advanced tools to China. Being friendly people, the Dutch complied, as part of the ASML supply chain, which was located in the US.

Not only are tool companies important to the Semiconductor Industry, but they are also a key geopolitical weapon and an important investment target for both professional and retail investors.

My hairdresser gives me a free haircut in return for the latest insights into the tools market. So if you see me with long hair (longer than 6mm), it is because the tool stocks are down, and I fear losing an ear in the snip seat.

While the Semiconductor Tool chain is as advanced as the semiconductors it produces, it can largely be categorised into front-end and back-end. The front-end tools are involved in transferring the chip design to silicon and creating a processed wafer, while the back-end tools are involved in mechanically processing the wafer into dies that are then tested and packaged.

While Semiconductor Tool companies can be involved in both front-end and back-end processing, they generally fall into one of the categories.

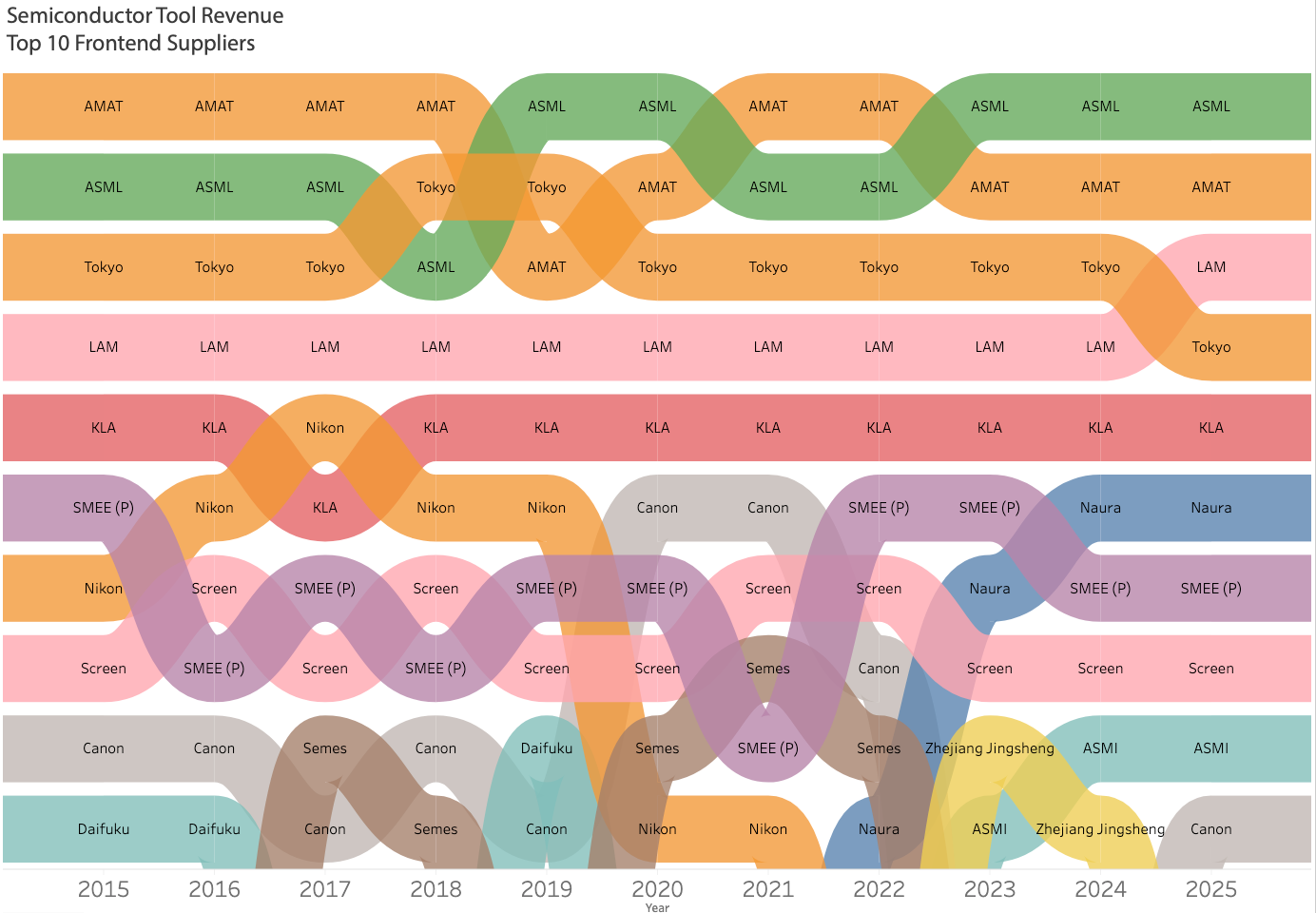

The top 10 Frontend tool companies can be seen below:

The top 5 front-end tool companies have been stable over the last decade, with ASML and AMAT holding the top spot. While Nikon briefly entered the top 5, the company has not had success with its lithography tools or the rest of its business, resulting in a significant writedown of its 3D metal printing assets.

The embargoes have given China an incentive to invest in a domestic semiconductor tool chain, and as a result, Naura has joined the SMEE as the second Chinese tool manufacturer in the top 10 for front-end tools.

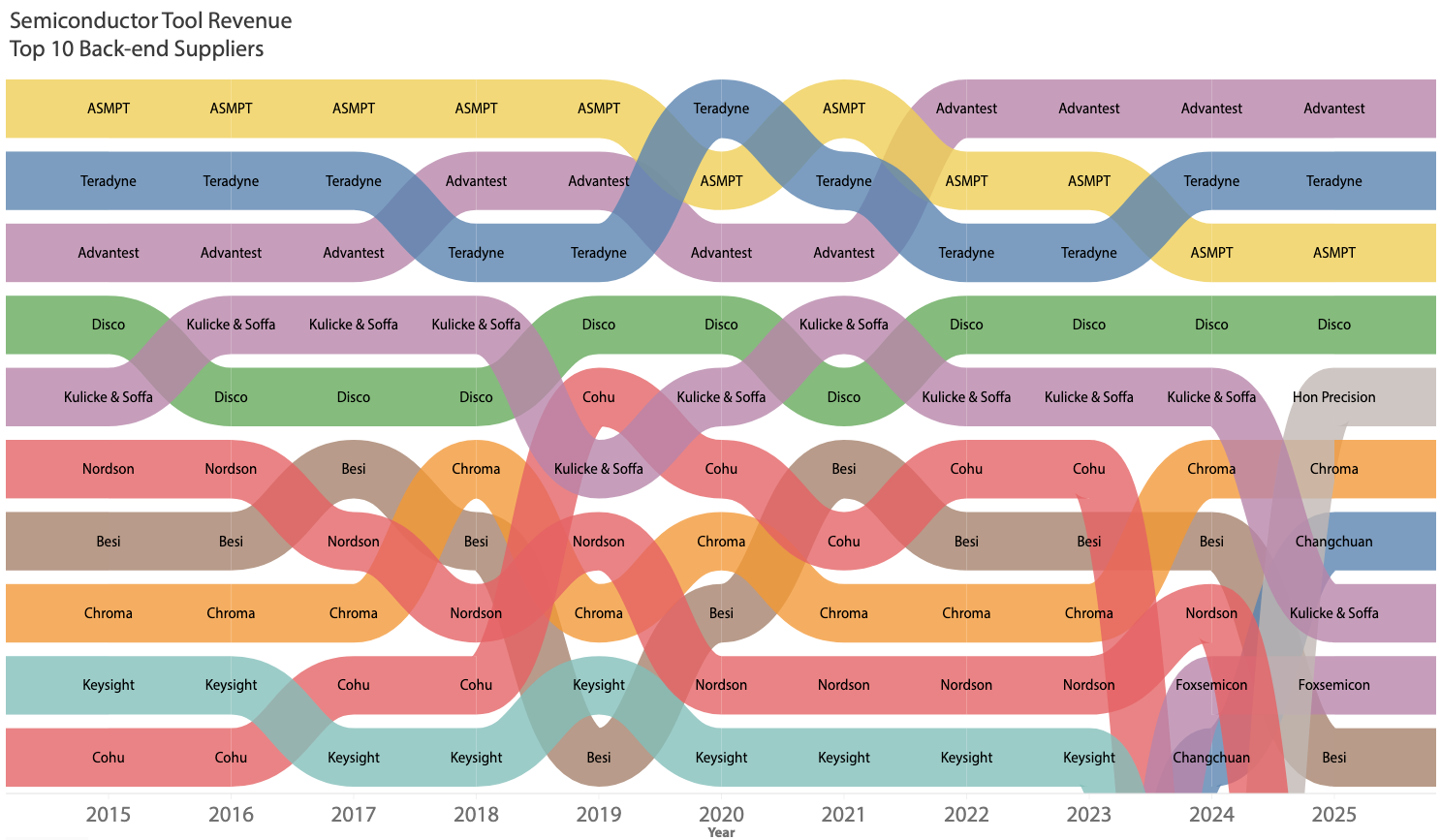

The top 10 back-end tool companies can be seen below:

The back-end tool companies have been shuffling more around, with the two test companies, Advantest and Teradyne, now firmly in the lead ahead of ASMPT, selling bonding and packaging tools.

Changhuan has joined the top 10 as the second Chinese back-end tool company, after ASMPT.

Most recently, the two Taiwanese companies Foxsmicon and Hon Precision have joined Chroma, bringing the total to 3 Taiwanese companies in the top 10.

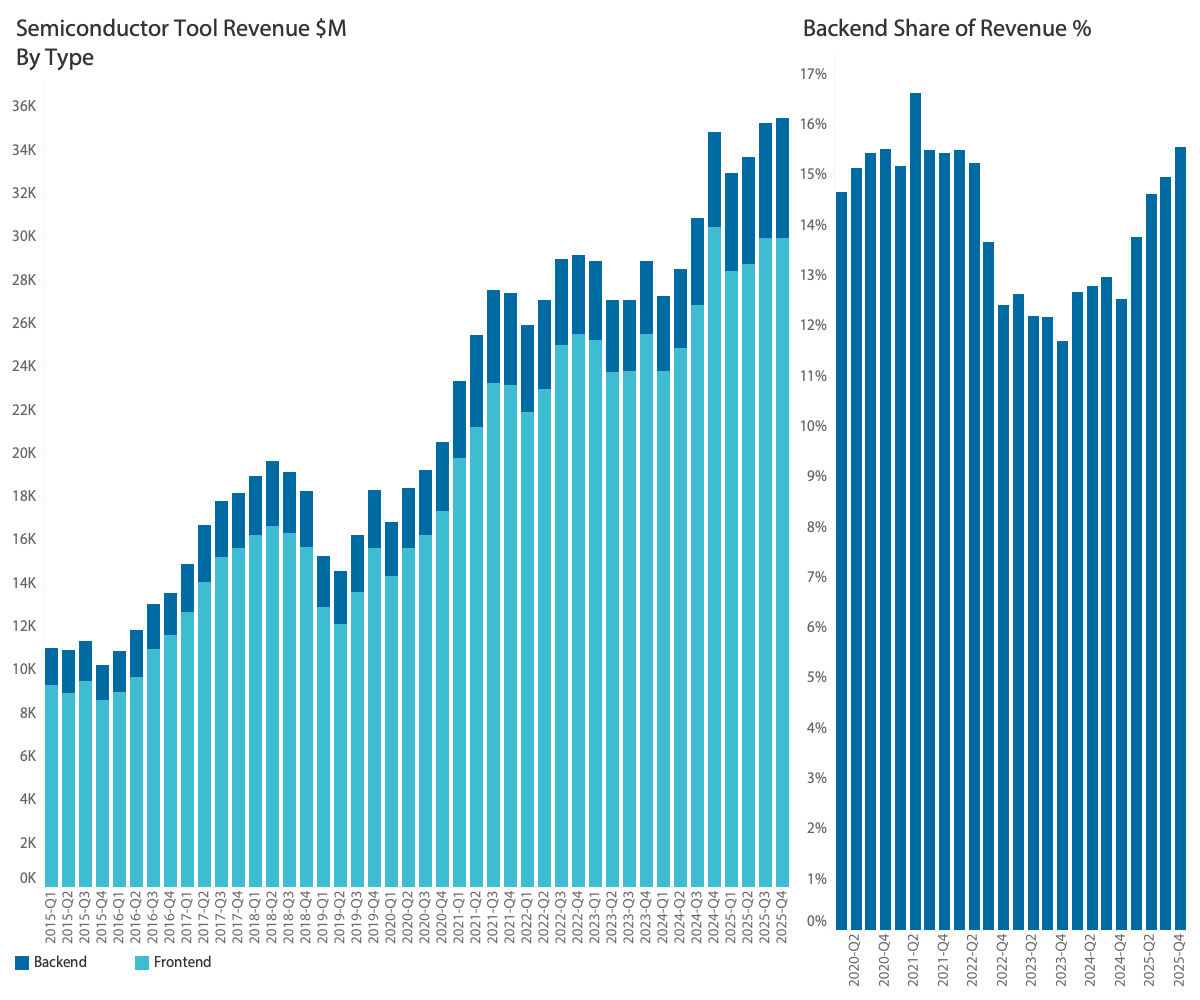

While the front-end tools generally get more attention than the back-end tools, the latter are growing faster.

The Back-end share of the tool revenue had been in decline since the beginning at 2021 and reached a low at the end of 2023. Since then, the share has grown from less than 12% to over 15.5% in the last quarter.

This trend began right after NVIDIA's first AI quarter, and that is no coincidence. While NVIDIA’s GPUs certainly require advanced semiconductors, they are less advanced than the M5 Mac I am writing this post on.

Many of the performance improvements introduced by the H100 and Blackwell were due to advanced packaging connectivity. Not only were the memories packaged with the GPU, but the High Bandwidth Memories (HBM) were also packaging marvels in their own right, using hybrid bonding to fuse the DRAM stacks before being mounted alongside the GPUs.

The new HBM and GPU packaging methods also involved more advanced, time-consuming testing, benefiting Advantest and Teradyne.

The Q4-2025 Results of Semiconductor Tools companies

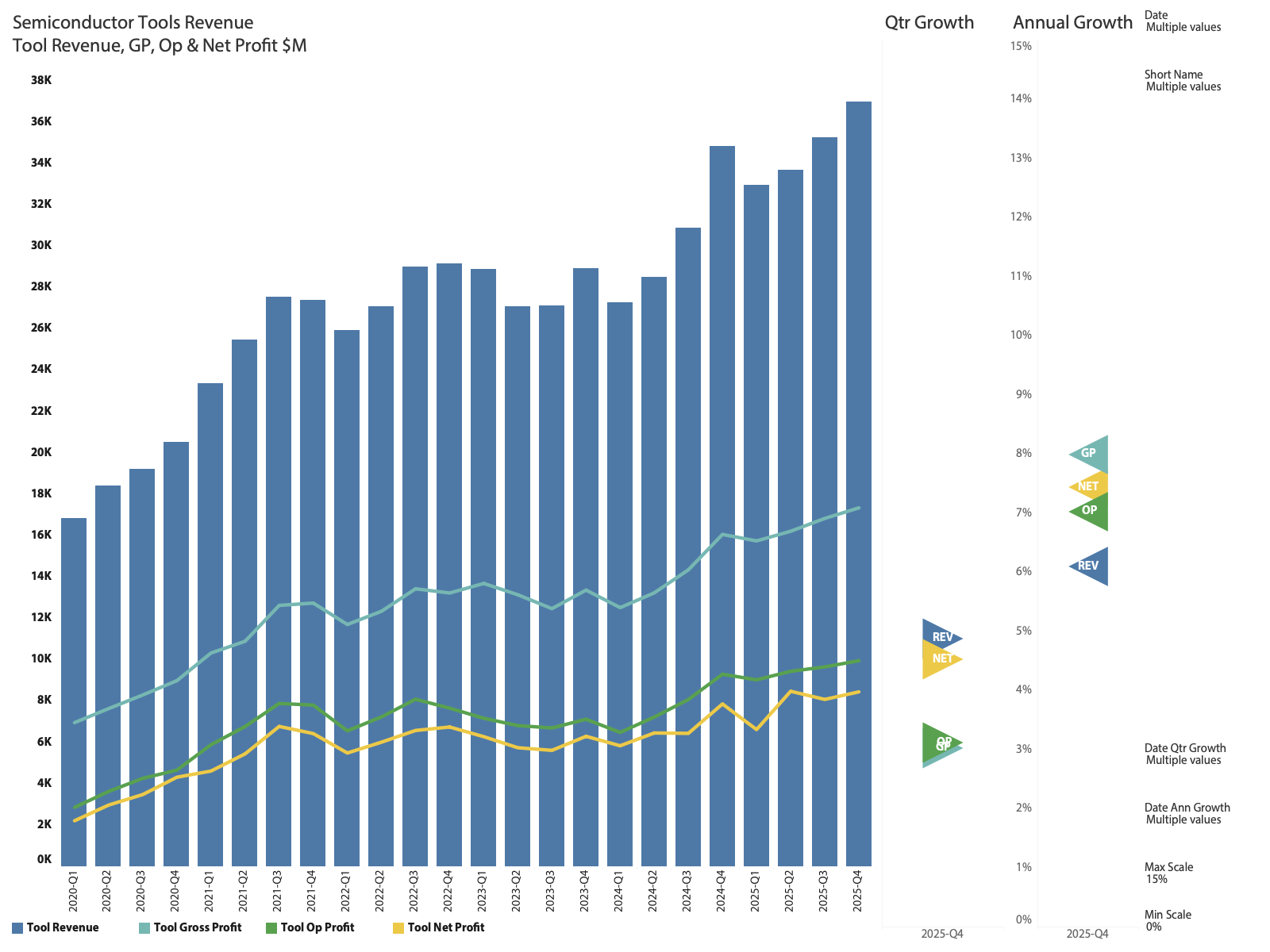

You might believe that Semiconductor Tool revenue was growing at a rate similar to that of Semiconductor companies, but no such luck. The current annual growth rate of Semiconductor Tools Revenue is a shade above 6%, well below the semiconductor growth rates currently in the twenties. This is also well below the 8% cross-cycle growth in semiconductor revenue.

Over the decade, tools and semiconductor revenue have had very similar growth rates, but they have become somewhat disconnected as chip money has been sprinkled across the industry.

It is worth noting that Tool revenue excludes service revenue, which has grown quite handsomely for the largest tool companies.

While much of the current semiconductor revenue is driven by profit, it is still somewhat surprising to see this modest growth rate, given that investments by large cloud companies at the end of the supply chain are growing at 72%.

All profits are outpacing revenue, suggesting that the tool companies operate in a controlled, highly predictable operational environment. I will cover supply and demand later in this post.

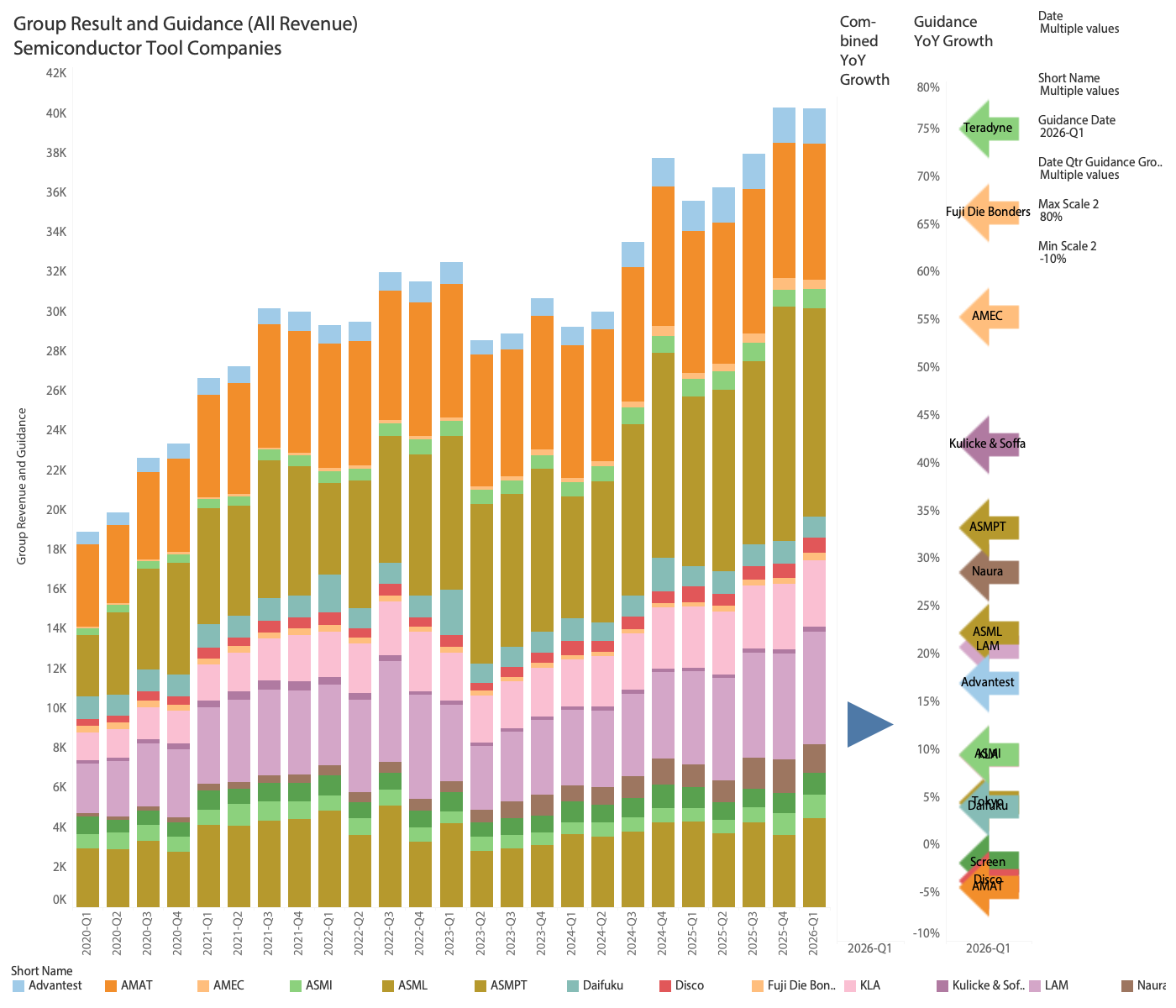

The short-term growth outlook for semiconductor tool companies can be analysed by examining the Q1-2026 guidance of the largest companies.

Guidance includes all revenue for the Semiconductor tool companies, including non-tool revenue, which is why I have excluded Canon and Nikon from the guidance analysis.

At 13% YoY growth, the guidance looks more positive for semiconductor tool companies, suggesting a flat Q1-2026, which is typically a seasonally weak quarter. The flat guidance should be compared to the last Q4-Q1 transition that was -6%

Once again, it looks like the back-end companies are leading the growth, with Advantest at a modest 17% YoY.

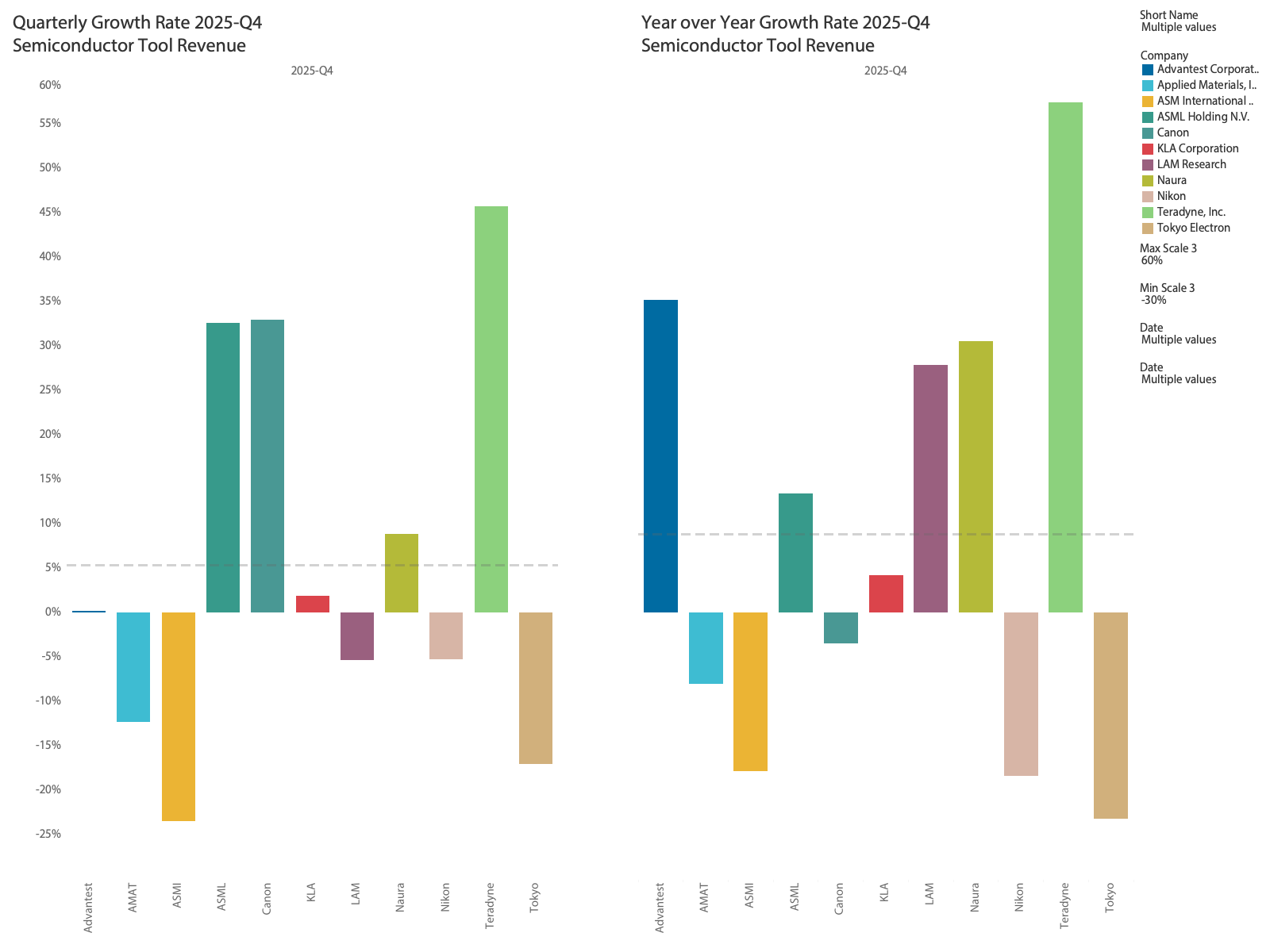

The individual company growth rates of the top companies show that Teradyne is in the lead, while Advantest is taking a breath after a significant growth period.

With a stronger year and quarter than AMAT, ASML is now pulling away as the top semiconductor tool company. In the second-tier lithography tools, Canon is doing better than Nikon. It is worth noting that Naura of China had a great year, once again highlighting that embargoes benefit the local Chinese tool companies.